> In 2025, steel mill profits experienced a comprehensive recovery.

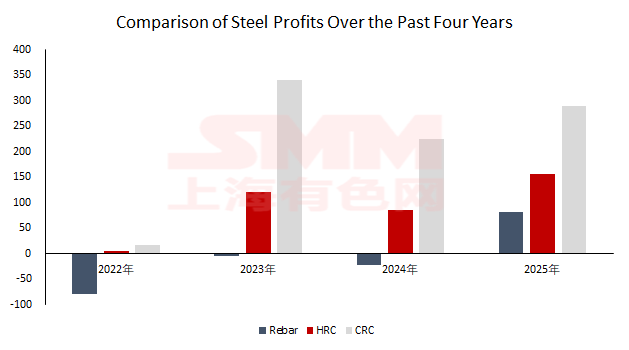

In 2025, steel mill profits improved significantly. According to SMM data, the average spot profit for rebar at blast furnace steel mills in east China was 82 yuan/mt, for hot-rolled coil 156 yuan/mt, and for cold-rolled coil 290 yuan/mt, with an average profit of 176 yuan/mt across these three products. In contrast, the average was 96 yuan/mt in 2024, 152 yuan/mt in 2023, and even -19 yuan/mt in 2022. It is evident that compared to the period from 2022 to 2024, steel mill profits achieved a full recovery this year.

> Steel mill profits expanded MoM in January

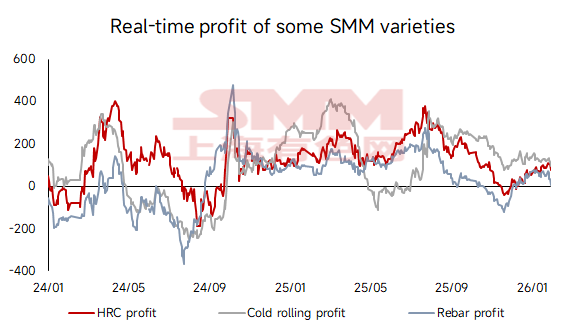

In January, raw material side, iron ore prices edged down rangebound, coke prices underwent several rounds of reductions, and steel scrap prices remained in the doldrums. Combined, these factors drove down the average steel mill costs by 1.3%.

Finished products side, entering January, end-use demand continued to weaken, and spot prices lacked upward momentum, leading to a marginal 0.3% decline in the average steel price. As raw material prices fell more sharply than steel prices, steel mill profits expanded MoM overall in January. Hot-rolled coil profits widened from around 31 yuan to 86 yuan, rebar profits increased from 20 yuan to 55 yuan, and cold-rolled coil profits fluctuated narrowly MoM on average.

Looking ahead, with the Chinese New Year approaching, market demand continues to weaken and trading activity gradually cools down. Both raw material and steel prices are expected to have limited room for fluctuation. Steel mill profits in February are likely to fluctuate rangebound compared to January, with little room for further expansion.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)